Written by Bobby Samuels

Edited by Arthur Goldgaber

Reviewed by Jovan Johnson, Esq., Structured Settlement & Annuity Specialist

Updated: April 9, 2026

The process of cashing out and selling your structured settlement may sound simple, but if you obtain three wildly different quotes for the same payments, it can become complicated very quickly. Complications arise because discount rates change weekly, judges ask different questions, and mystery fees appear out of nowhere.

So how do you determine what your payments are actually worth and who’s offering you a fair deal?

First, let’s examine the fundamentals.

The Fundamentals: What Is a Structured Settlement?

Before you can sell something, you must know what you have. A structured settlement is a legal financial arrangement that provides you with compensation through scheduled payments over time, instead of one giant check.

Most settlements are negotiated as a result of personal injury lawsuits, medical malpractice claims, wrongful death cases, or workers’ compensation settlements. The payments are also tax-free and funded through annuities, an insurance product guaranteeing fixed payments on a set schedule.

What Are You Actually Selling?

In a structured settlement, you’re selling the legal right to receive future payments. A factoring company (the “buyer”) gives you cash now, and they collect your scheduled payments later on.

The catch? The factoring company doesn’t pay you the full value of those future payments. They apply a discount rate, typically between 9% and 18%, reflecting the present value of those your future payments.

For instance, if you’re scheduled to receive $100,000 over 10 years, you might receive $65,000 to $75,000 in cash today. The gap covers their profit, transaction costs, and the time value of money.

However, it’s worth stressing that none of this happens without court approval.

Reasons to Consider Selling Your Annuity Payments

Consider the following scenarios:

- Medical Bills Piling Up: Hospital bills and ongoing treatment costs don’t wait for your next scheduled payment. Selling a portion can eliminate high-interest medical debt before it lowers your credit score.

- Home Down Payment: Renting costs more over time than purchasing a home, but a down payment requires cash upfront. Trading future payments for equity can make financial sense if the numbers work.

- Business Investment: Starting or saving a business often requires capital quickly. Your monthly $800 payment won’t suffice if you need $30,000 to keep the doors open and the lights on.

- Education Costs: Student loans charge interest while you wait for payments. Funding school tuition and other costs now can mean less debt later, especially for career-changing degrees.

- Debt Consolidation: Credit cards that charge an annual percentage rate (APR) of 24% APR will eat you alive. Selling enough to wipe out high-interest debt can save thousands in the long run.

- Significant Life Changes: Divorce settlements, relocations for work, or unexpected funeral costs may exceed your monthly payment schedule. Sometimes life forces your hand.

Who Can Benefit from Selling Annuity Payments?

If those monthly payments cover basic expenses, such as rent and food, selling them for cash you’ll burn through in six months will leave you worse off than where you started. But for specific goals—especially time-sensitive opportunities— selling can solve problems that waiting can’t.

- People Drowning in High-Interest Debt: Credit card interest at 24% compounds daily. If your structured settlement payments stretch out for years while debt multiplies, selling makes mathematical sense.

- Homebuyers and Renovators: First-time buyers who need down payment money or homeowners facing major repairs (i.e., a new roof, or foundation work) benefit from converting future payments into immediate equity.

- Entrepreneurs and Small Business Owners: Business opportunities have expiration dates. Waiting 18 months for enough payments to fund expansion can lead to competitors grabbing your market share.

- Career Changers and Students: Retraining for a new field or finishing a degree requires tuition money now, not later. Trading payments for education can increase earning power faster than waiting.

- Medical Emergency Cases: Treatments, surgeries, or long-term care needs generally can’t be paid on an installment plan; they must be paid in full when the bill arrives. . Selling avoids piling medical bills on credit cards at predatory rates.

- People Who Hate Managing Monthly Payments: Some folks prefer simplicity. One lump sum to invest or manage beats tracking payments for decades, especially if you have better investment opportunities.

Options for Selling Annuity Payments

Knowing you need cash is step one. However, deciding how much to sell requires strategy. You don’t have to dump your entire payment stream for a lump sum. Most people assume it’s all or nothing, but you have three options that let you match the sale to your financial situation.

- Full Sale: You sell every future payment in exchange for one lump sum now. You get the most cash upfront, but give up all future income from the annuity. Full sales make sense when you have other income sources or need maximum capital for something like starting a business or paying off substantial debt.

- Partial Sale: You sell a chunk of your future payments and keep the rest. Maybe you will sell the next five years of payments but keep everything after that, or you will decide to sell half of each future payment. You get cash now while preserving some future income, which works well when you need to fund a down payment but you still want monthly checks for living expenses.

- Specific Dollar Amount: You tell the buyer exactly how much cash you need, and they calculate which payments they must buy to give you that amount. Need $35,000 for medical bills? They’ll figure out whether that means selling your next 18 months of payments or a percentage of payments over several years. You solve your immediate problem without overselling and leaving money on the table.

What Determines Your Payout?

Choosing which payments to sell is half the battle. The other half is understanding why one buyer offers you $65,000 while another proposes $72,000 for the exact same payment stream.

Discount Rate

The discount rate reflects the profit a buyer builds into the deal. The buyers apply this rate to your future payments to calculate what they’ll pay you today; lower rates mean more cash in your pocket now.

Most buyers apply a discount rate between 9% and 18%, but you may be offered quotes outside that range, depending on the company and your payment structure. Someone quoting you a discount rate of 15% will pay you thousands less than someone at 10% for identical payments.

It’s prudent to always obtain multiple quotes and demand line-item breakdowns showing exactly how the buyer calculated your offer. Buyers who refuse to show their math are hiding something.

Payment Schedule

Payment timing changes everything. Buyers pay more for payments arriving soon, in large chunks, and with iron-clad guarantees. For example, a $50,000 payment arriving next year is worth more than the same payment arriving in 10 years.

Consider the following as well:

- Larger payments spread your transaction costs over more dollars, which improves your rate.

- Guaranteed payments beat life-contingent payments because there’s zero death risk for the buyer.

- Small deals and payments tied to your lifespan typically are assessed with higher discount rates because the risk-to-reward ratio works against you.

Present Value: What Future Money Is Worth Today

Present value answers one question: what would you pay today to receive a specific dollar amount later? Money you get next year is worth less than money in your hand right now because you lose the chance to invest it, and inflation erodes purchasing power.

The standard formula for calculating the present value of an annuity is:

PV = PMT × [(1 – (1 + r)^-n) / r]

Where:

- PV = Present Value (what the buyer pays you)

- PMT = Your payment amount

- r = Discount rate per period

- n = Number of payments

So, let’s say you have 60 monthly payments of $1,000 each, totaling $60,000. At a 12% annual discount rate (1% monthly), the present value is $44,955. That’s what a buyer using that rate would offer you.

Drop the discount rate to 9% annually (0.75% monthly), and the present value jumps to $48,173.

The $3,218 difference is pure profit margin that can be negotiated.

Other Factors That Affect Your Offer

- Interest Rate Environment: When prevailing interest rates climb, discount rates usually rise in tandem. Buyers adjust their rates based on what they can earn elsewhere, so your payout shrinks when rates are rising.

- Payment Characteristics: Size matters, frequency matters, and how many payments remain matters. Selling 120 monthly payments of $500 each is priced differently from selling 10 annual payments of $6,000, even though both total $60,000.

- Guarantees vs. Life-Contingent Features: Payments guaranteed for a set period command better rates than payments that stop if you die. Buyers hate uncertainty, and life-contingent features introduce mortality risk that they’ll charge you for.

- Issuer Quality and Documentation: Clean paperwork from a reputable insurance company usually obtain better rates than messy files from sketchy sources. Buyers pay more when they can verify everything quickly.

- Deal Size and Legal Costs: Selling $10,000 in payments costs nearly as much to process as selling $100,000. Smaller deals carry proportionally higher effective rates because fixed costs account for a bigger percentage of the deal.

- State Requirements and Court Calendars: Some states have stricter approval processes than others. Backed-up court calendars delay closing and increase holding costs for buyers, which they pass on to you through lower offers.

The Sale Process: From Quote to Cash

Understanding what drives your offer is useless if you don’t know how to turn that offer into actual money in your bank account. The process involves more steps than just signing papers and cashing a check. Due to vetting buyers, negotiating rates, and getting legal approval, at the process may take 30 to 180 days, depending on your state and whether you’re selling a structured settlement or a commercial annuity.

Step 1: Research Buyers and Verify Credibility

Big advertising budgets don’t equal trustworthy companies.

Start by checking financial strength ratings from AM Best or Fitch Ratings. Aim for companies rated A- or higher, which signals they can actually pay what they promise. Pull up their complaint index score from the NAIC website. Scores of 1.0 or lower mean minimal complaints. Anything higher suggests problems you don’t want to inherit. Check Better Business Bureau reviews as well to ascertain how they handle disputes.

Some buyers ghost you after the sale closes. Others answer calls and fix mistakes. Talk to your accountant or financial planner if you have one. The outside perspective catches red flags that you might miss.

Step 2: Contact Multiple Buyers and Get Free Quotes

Call at least three companies and ask for free quotes. The quality of customer service tells you everything. Representatives who explain options clearly without pressure are keepers. Those who rush you or dodge questions are trying to hide unfavorable terms.

Ask every buyer the same questions: Can you change your mind after signing? What fees will be tacked on? How long until you get paid? What documents do you need? What is the quote’s expiration date? Write down their answers and compare them side by side.

Quotes expire quickly, usually within 30 to 60 days, because discount rates shift with market conditions. Never accept the first offer without shopping around.

Step 3: Evaluate Offers and Negotiate Your Rate

Your discount rate depends on payment timing, deal size, and how badly the buyer wants your business. Lower rates mean more money for you. Someone quoting 15% will pay thousands less than someone at 10%.

If the best offer still feels low, negotiate. Buyers expect it. Point to better rates from competitors and ask them to match or beat it.

The worst they can say is no, and you’re back where you started.

Step 4: Complete Required Paperwork

Once you accept an offer, the paperwork starts piling up.

You’ll need two forms of ID, a completed application, your original annuity or settlement contract, and a release agreement. Missing documents delay everything, sometimes by weeks.

Keep copies of every document in a folder you can access easily. For commercial annuities, the buyer and insurance company handle most processing, which takes about four weeks.

Structured settlements add court filing requirements handled by an attorney, either one you hire or one provided by the factoring company. Submit everything on time and respond to requests quickly.

The longer the paperwork sits on your desk, the longer your money stays in their account.

Step 5: Wait for Approval

Insurance companies that issued your annuity must approve the sale. They verify the buyer is legitimate and that the transaction follows contract terms.

Assuming everything checks out, approval is straightforward. Some states require third-party assessments of the sale terms. Others give you a cooling-off period to change your mind. Check your state’s rules and regulations with a lawyer or financial advisor before signing the final documents.

Step 6: Get Court Approval (If It’s a Structured Settlement)

Structured settlements differ from commercial annuities because they require one final step: court approval.

At the end of the day, courts want to confirm you’re not making a decision that may bankrupt you and make you dependent on public assistance. They also operate under Structured Settlement Protection Acts, state laws designed to protect sellers from predatory buyers.

Step one is returning your signed documents. An attorney will then file paperwork to schedule a hearing. At the hearing, you’ll then explain why you need the money and prove the sale won’t wreck your financial future. Judges evaluate your employment situation, the buyer’s reputation, the discount rate you’re getting, and whether you’ve sold payments before.

Once the judge approves, the transfer order goes to the insurance company. Funds are transferred to your account as fast as state law allows, usually within a few days.

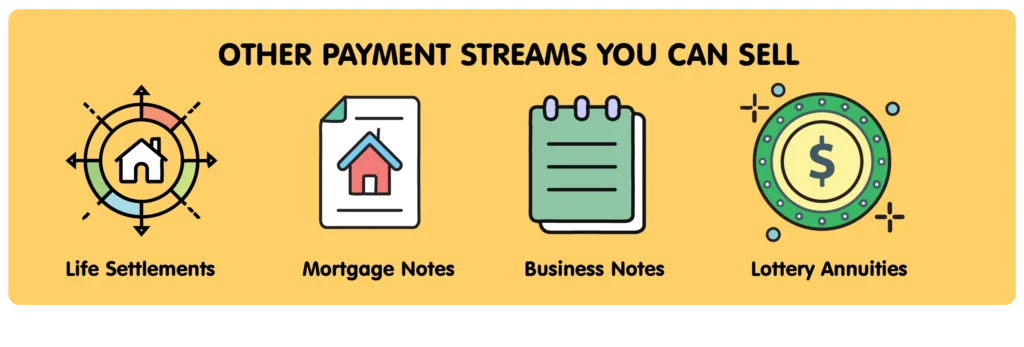

Beyond Annuities: Other Payment Streams You Can Sell

Structured settlements and annuities aren’t the only payment streams buyers want. Each payment type has its own quirks, timelines, and legal hoops, but the core concept stays the same. To obtain cash now, you must sell your future payments at a discount.

Life Settlements (Selling a Life Insurance Policy)

You can sell an unwanted life insurance policy for more than its cash surrender value but less than the death benefit. The buyer takes over the premium payments and collects the death benefit when you die. The process typically takes 60 to 90 days, and fraud prevention rules require medical records and policy verification to keep scammers out of the market.

Mortgage Notes

Holding a mortgage note from a property you sold means you’re the bank collecting monthly payments. You can sell the entire note or just a portion of future payments. Buyers price this based on the borrower’s credit, the interest rate, the loan-to-value ratio, the property value, and how clean your documentation is. Expect a discounted offer that accounts for default risk and present value calculations.

Business Notes (Seller-Financing Notes)

Seller-financed a business sale, and now you’re stuck waiting for payments? You can sell that note. The value depends on payment history, the buyer’s financial health, any guarantees backing the note, and the yield rate demanded by the buyers. A robust payment history and solid guarantees lower the discount rate and boost your payout because buyers are exposed to less risk.

Lottery and Sweepstakes Annuities

Did you win the lottery and are now receiving annual payments? Most states permit you to sell those payments, but state lottery regulations, tax implications, and court approval requirements vary considerably. Some states make it nearly impossible; others rubber-stamp sales with minimal scrutiny. You must check your state’s specific rules before assuming you can cash out, and consider whether keeping the annuity beats taking a discounted lump sum.

Pensions and Other Streams

Federal pensions can’t be sold, period. Some private pensions allow limited transfer options at or after full retirement age, but most have strict regulations preventing sales. Plan documents and federal law create barriers that don’t exist with annuities or settlements. Always verify your specific plan’s rules and legal constraints before wasting time getting quotes that go nowhere.

Frequently Asked Questions (FAQs)

How do you sell your annuity?

Research multiple buyers, get free quotes, compare discount rates, accept the best offer, complete paperwork, and wait for approval. Commercial annuities need insurance company approval, while structured settlements require court approval.

How long will it take to sell?

Commercial annuities take 45 to 60 days on average. Structured settlements take 30 to 180 days because of court approval requirements. Backed-up court calendars, missing documents, and unresponsive buyers stretch timelines. States with stricter consumer protection laws require additional steps and time.

Do I need court approval?

Structured settlements always require court approval due to Structured Settlement Protection Acts. Judges must confirm the sale serves your best interest. Commercial annuities skip court and only need insurance company approval. The difference comes down to how the annuity was created and funded.

Is this taxed?

Structured settlement sales usually aren’t taxed at the seller level because you’re transferring ownership of tax-free payments. Commercial annuity sales have different tax treatment depending on how the annuity was funded and whether you’re withdrawing or selling. Talk to a tax professional before signing anything because your specific contract and state law create exceptions.

What if the buyer skips court approval?

Federal law slaps a 40% excise tax on buyers who skip required court approval for structured settlement transfers. The penalty protects you by forcing buyers to follow the regulations. If a buyer suggests skipping court to expedite things, walk away. They’re either incompetent or crooked.

Take the Next Step: Reach out to Annuity Payment Freedom

Questions about selling your payments? Want to know if we can help with your specific situation? Please reach out by phone or email.

Call Us: (877) 547-3672

You can talk to a knowledgeable customer service representative who can answer questions, explain your options, and help you understand what your payments are worth. No commitment required.

Email Us: hello@annuityfreedom.com

SOURCES:

- https://www.forbes.com/sites/jeremybabener/2025/02/07/record-use-of-structured-settlements-offering-safety-and-returns/

- https://www.4structures.com/sell-structured-settlement-information

- https://www.nasp-usa.com/secondary_market_faq.php

- https://www.principal.com/individuals/build-your-knowledge/whats-59-half-rule-early-retirement-savings-withdrawals

- https://www.law.cornell.edu/uscode/text/26/5891

- https://ncoil.org/wp-content/uploads/2016/12/model-struc-settlement.pdf

- https://www.fdic.gov/bank-examinations/senior-life-settlements-cautionary-tale

About the Author: Jovan Johnson, Esq. is a structured settlement & annuity specialist with 12 years of experience, based in California. He has also practiced as an attorney in consumer and small business bankruptcy and debt settlement. Annuity Freedom has been helping clients sell annuity payments since 2017.